- Trump tariffs and CBAM represent different strategies: U.S. protectionism vs. EU carbon accountability.

- Trump tariffs aim to protect domestic industry, while CBAM tackles carbon emissions, impacting global supply chains.

- Both tariff systems have winners and losers, reshaping trade dynamics and competitiveness.

- Industries must adapt for survivability by aligning with low-carbon initiatives and exploring new markets.

- New policies call for businesses to innovate and strategize for a sustainable future.

Tariffs have always been a tool of economic warfare—changing market dynamics, influencing trade relationships, and defining competitive advantages.

But today, the game is changing.

Two of the most significant trade policies in recent years—Trump's steel and aluminum tariffs and the EU’s Carbon Border Adjustment Mechanism (CBAM)—highlight a new kind of trade war.

One is textbook protectionism, which inflates costs to boost the domestic industry. The other is a carbon accountability system, realigning global supply chains to favour low-emission production.

Where do businesses stand in this new reality? More importantly, who wins, who loses, and how can companies future-proof themselves?

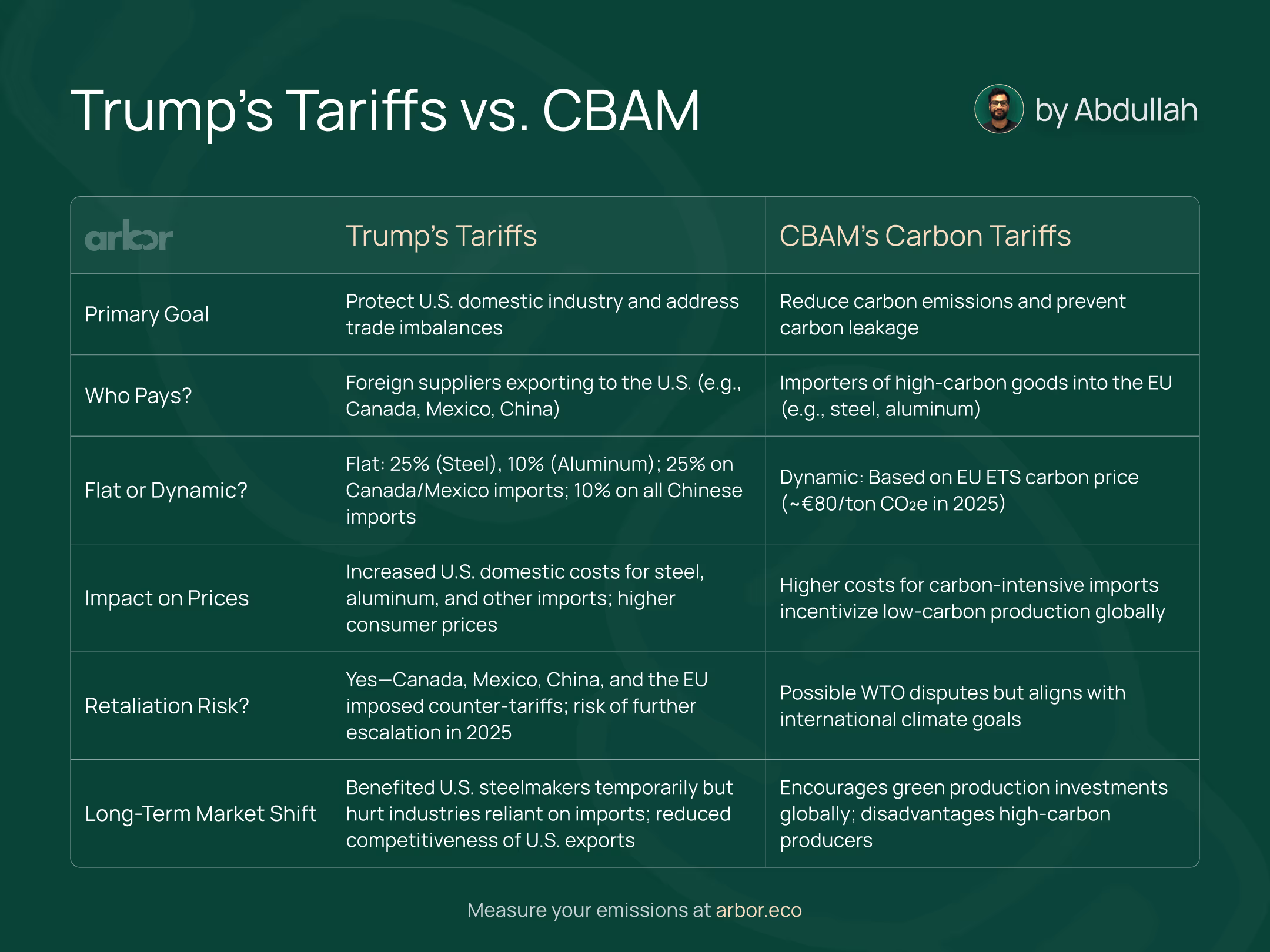

Trump’s Tariffs vs. CBAM: A Side-by-Side Comparison

Comparing the impact of United States leader, Donald Trump’s tariffs against the European Union’s Carbon Border Adjustment Mechanism (CBAM) regulatio.

Here's a fancy image comparing the two:

Take the tariff quiz

Trump’s tariffs

Overview of the tariffs

- What? A series of tariffs imposed on various countries and products, including:

- 25% on steel and 10% on aluminum imports

- 10% on all imports from China

- 25% on most imports from Canada and Mexico, with 10% on Canadian energy resources

- Why? To protect U.S. manufacturers, address trade imbalances, enhance national security, and tackle issues like the opioid crisis and border security.

- When? New tariffs were proposed in early 2025.

- Effect?

- Increased prices for U.S. consumers and industries reliant on imports

- Retaliation from affected countries leads to trade tensions

- Disruption of global supply chains

- Potential job losses in some sectors and gains in others

- Reshaping of international trade relationships and dynamics

These wide-ranging tariffs represent a significant shift in U.S. trade policy, with far-reaching consequences for the global economy and international relations.

Steel & aluminum tariffs

- What? A flat 25% import duty on steel and 10% on aluminum was imposed under the guise of national security.

- Why? To protect U.S. manufacturers from foreign competition, particularly China and Canada.

- Effect? Local prices soared for U.S. industries reliant on imports, passing costs down the supply chain. Retaliation from Canada, Mexico, and the EU is creating further tensions.

CBAM (Carbon Border Adjustment Mechanism)

- What? A border tax on high-carbon imports (steel, aluminum, cement, etc.), pegged to the EU’s carbon price (currently ~€80/ton CO₂e).

- Why? To prevent “carbon leakage,” where companies move production to regions with weak regulations.

- When? 2026 Implementation. See more on the EU’s CBAM and the UK’s CBAM.

- Effect? Higher costs for carbon-intensive producers exporting to the EU. A pricing advantage for already decarbonized companies, making low-carbon steel and aluminum more competitive.

These policies reshape supply chains, but they produce distinctly different winners and losers.

The biggest winners

1. U.S. and EU domestic producers

- Trump’s tariffs gave U.S. manufacturers an artificial pricing edge, at least temporarily.

- CBAM rewards EU producers already subjected to carbon costs, protecting them from cheaper, high-emission imports.

2. Low-carbon steel & aluminum producers

- Companies investing in Electric Arc Furnaces (EAFs) and renewable energy-powered smelting (like Swedish-based H2 Green Steel) now have a direct cost advantage in the EU.

- Hydrogen-powered aluminum smelters are next in line to benefit from CBAM.

3. Carbon-accountable regions (Norway, Sweden, Canada’s hydro-based sector)

- Norwegian and Swedish steelmakers, already adopting green production methods, see new market opportunities in the EU.

- Canada’s hydro-powered aluminum sector (Quebec in particular) is at a competitive advantage for CBAM-covered exports.

The biggest losers

1. Canada & Mexico (Trump's trade policies)

Canada and Mexico got caught in the crossfire of Trump’s tariffs despite being top trading partners, as their steel and aluminum exports to the U.S. suddenly became significantly more expensive for American buyers due to the added cost of the tariffs.

What happened?

- Canadian steel & aluminum exports to the U.S. tanked.

- Mexico had to rethink production strategies, driving increased focus on domestic markets.

- Both faced immediate retaliatory tariffs, escalating prices in everything from agriculture to automotive.

2. High-emission producers selling to the EU (CBAM)

If you're a coal-powered steel producer in China, India, or Russia, CBAM is a nightmare.

The pain points:

- Chinese and Indian blast furnaces are among the most carbon-intensive globally 🌎.

- Retrofitting or transitioning to low-carbon production takes time and capital—companies that don't are locked into CBAM's extra cost.

- Russia, once a major player in EU steel exports, is seeing barriers grow.

Key takeaway: If you’re producing CO₂-intensive steel or aluminum, CBAM is a regulatory freight train running straight through your business model.

How can losers adapt?

There is a way out for businesses stuck between higher tariffs and changing policies—adaptation and realignment.

1. Canada & Mexico’s playbook

With Trump-era tariffs making U.S. markets unstable, Canada and Mexico should pivot toward the EU, strategically aligning themselves with CBAM regulations.

✅ Leverage low-carbon supply chains.

- Canada’s hydro-powered aluminum has a huge opportunity for EU exports.

- Mexico could position itself as a low-carbon alternative, investing in cleaner production for CBAM alignment.

✅ Capitalize on sustainable finance opportunities.

- Canadian and Mexican firms can seek green financing options to retrofit plants, lower emissions, and ensure future competitiveness.

✅ Strategic trade partnerships.

- New trade deals with the EU (or other pro-climate regions) could help offset losses in the U.S.

2. Coal-Based Producers (China, India, Russia) Need a Reality Check

- Pivot away from outdated blast furnaces

- Invest in hydrogen-based steelmaking (following models like Sweden’s SSAB)

- Enter into PPAs (Power Purchase Agreements) to use renewable energy in refining operations

Bottom line: The laggards in this transition will get priced out of critical markets. Speed matters.

Tariffs are no longer just about trade—they’re about transformation

Trump’s tariffs inflated prices but don’t drive long-term innovation. CBAM, by contrast, forces a rethink of how materials are produced, measured, and valued.

Businesses that embrace these new rules—not just in the EU but anticipating similar policies elsewhere—will win the long game.

Those who resist? Well, they'll pay the price. Is your business ready for the shift?

Let’s make it happen. Measure your emissions with Arbor.

Measure your carbon emissions with Arbor

Simple, easy carbon accounting.

.webp)

%20Directive.webp)

.webp)

%20Arbor.avif)

%20Arbor.avif)

.avif)

%20Arbor%20Canada.avif)

.avif)

%20Arbor.avif)

.avif)

_.avif)

.avif)

%20Arbor.avif)

%20Software%20and%20Tools.avif)

.avif)

.avif)

%20EU%20Regulation.avif)

.avif)

%20Arbor.avif)

_%20_%20Carbon%20101.avif)

.avif)